The Provident Fund (PF) is one of the most significant retirement savings instruments available to salaried employees in India. While withdrawing PF funds may appear to be a convenient solution during financial emergencies or job transitions, such withdrawals can have long-term implications on your retirement planning and financial security.

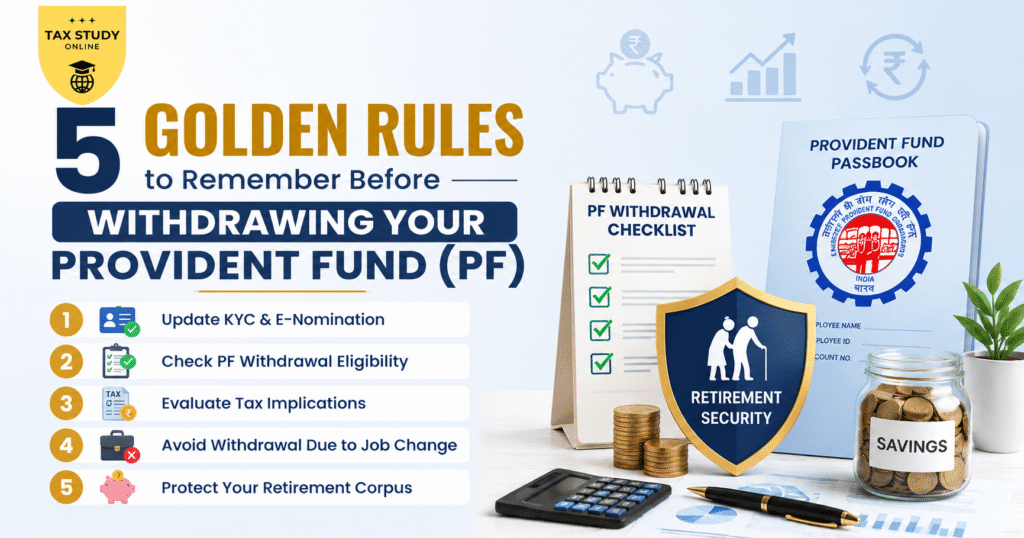

Before submitting a PF withdrawal claim, it is important to keep the following five golden rules in mind.

1. Ensure Your KYC and E-Nomination Details Are Updated

Before initiating a PF withdrawal, verify that your Aadhaar, PAN, bank account details, and mobile number are linked and authenticated with your EPF account. Incomplete or incorrect KYC information is one of the primary reasons for claim delays and rejections.

Additionally, members should update their e-nomination details. A valid nomination ensures a smooth and hassle-free settlement process for family members in unforeseen circumstances.

2. Understand Your Eligibility for PF Withdrawal

The Employees’ Provident Fund Organisation (EPFO) permits both full and partial withdrawals, subject to specific eligibility conditions.

Full PF Withdrawal

A member may generally withdraw the entire PF balance under the following circumstances:

- Retirement from service.

- Attainment of the prescribed retirement age and cessation of employment.

- Continuous unemployment for the period prescribed under prevailing EPFO regulations. Currently, members may withdraw up to 75% of their PF balance after job loss, while the remaining balance can be withdrawn after 12 months of continuous unemployment, subject to applicable rules.

- Permanent migration abroad.

- Permanent disability resulting in the inability to continue employment.

Partial PF Withdrawal

EPFO also allows partial withdrawals (advances) while the member remains employed for specified purposes, including:

- Medical treatment for self or family members.

- Higher education.

- Marriage expenses.

- Purchase, construction, or renovation of a residential property.

- Other special circumstances as permitted under EPFO regulations.

3. Evaluate the Tax Implications Carefully

Taxation is an important factor to consider before withdrawing your PF balance. Although PF enjoys significant tax benefits during the accumulation phase, premature withdrawal may result in tax liability.

The Five-Year Rule

The tax treatment of PF withdrawals depends largely on the duration of continuous service:

- Withdrawal after five years of continuous service: The entire PF withdrawal amount is generally exempt from income tax.

- Withdrawal before completing five years of continuous service: Tax Deducted at Source (TDS) is applicable at 10%, provided PAN is furnished and linked. In the absence of PAN, TDS may be deducted at 20%, subject to applicable provisions.

4. Avoid Withdrawing PF Merely Due to a Job Change

A change of employment should not be considered a reason for withdrawing your PF balance. Instead, employees should transfer their existing PF accumulation to the PF account associated with their new employer through the EPFO online portal using their Universal Account Number (UAN).

Transferring the PF balance helps maintain continuity of service, preserves tax benefits, and allows retirement savings to continue growing without interruption.

5. Consider the Impact on Your Retirement Corpus

The primary objective of the Provident Fund is to build a retirement corpus over the long term. An early withdrawal not only reduces the principal amount accumulated but also eliminates the opportunity to earn future interest on that amount.

Even a relatively small withdrawal today can significantly reduce the value of your retirement savings over time due to the loss of compounding benefits. Therefore, PF withdrawals should be considered only after carefully evaluating their long-term impact on your financial security and retirement goals.

Conclusion

Your Provident Fund is more than just a savings account—it is a crucial component of your retirement planning. Before making a withdrawal, ensure that you understand the eligibility conditions, tax implications, and long-term consequences. Making informed decisions today can help secure a stronger financial future tomorrow.

Frequently Asked Questions (FAQs)

1. Can I withdraw my entire PF balance immediately after leaving a job?

No. Under current EPFO regulations, a member can withdraw up to 75% of the PF balance after becoming unemployed. The remaining balance may generally be withdrawn after 12 months of continuous unemployment, subject to applicable EPFO rules and conditions.

2. Is PF withdrawal taxable?

PF withdrawal is generally tax-free if the employee has completed at least five years of continuous service. However, withdrawals made before completing five years of continuous service may attract tax and TDS, subject to certain exceptions provided under the Income Tax Act.

3. Can I withdraw PF while I am still employed?

Yes. EPFO permits partial withdrawals (advances) during employment for specific purposes such as medical treatment, higher education, marriage expenses, home purchase, home construction, or house renovation, subject to eligibility criteria.

4. What should I do with my PF account when I change jobs?

Instead of withdrawing your PF balance, you should transfer it to your new employer’s PF account using your Universal Account Number (UAN). This helps maintain continuity of service and preserves long-term retirement benefits.

5. What documents are required for a smooth PF withdrawal process?

To ensure timely processing of your claim, your EPF account should have updated and verified KYC details, including Aadhaar, PAN, bank account information, and mobile number. Additionally, maintaining an updated e-nomination is highly recommended.