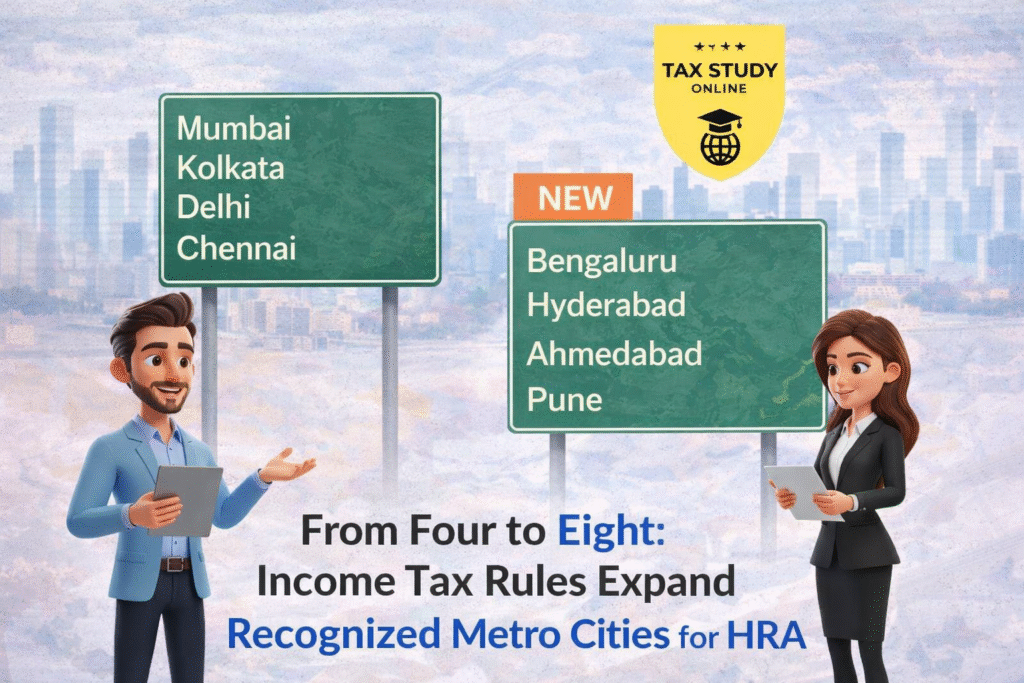

In a landmark update for salaried taxpayers, the Income Tax Rules have expanded the list of recognized metropolitan cities for the purpose of calculating House Rent Allowance (HRA) exemption. What was previously limited to four traditional metro cities has now been broadened to eight – bringing substantial tax relief to employees residing in India’s rapidly growing urban hubs.

This revision reflects changing economic realities, rising rental costs, and the expanding footprint of India’s metropolitan economies.

Let’s examine the change in depth and understand its financial, practical, and policy implications.

The Earlier Position: Only Four Metro Cities

Under the earlier framework, only the following cities were treated as metro cities for HRA calculation:

- Delhi

- Mumbai

- Kolkata

- Chennai

Employees living in these cities were allowed to compute HRA exemption using 50% of salary as the upper threshold.

For all other cities, the limit was restricted to 40% of salary, regardless of actual rental pressures.

Over time, this classification became outdated as several emerging cities witnessed comparable rental inflation and population density.

The New Expansion: Four Additional Cities Included

The updated Income Tax Rules now recognize the following cities as metro cities for HRA purposes:

- Ahmedabad

- Hyderabad

- Pune

- Bengaluru

With this revision, the number of recognized metro cities has doubled – from four to eight.

This move acknowledges their:

- Rapid urban expansion

- Significant rental cost escalation

- Economic importance

- High concentration of salaried professionals

Understanding HRA Exemption: A Detailed Breakdown

HRA exemption is calculated as the least of the following three amounts:

- Actual HRA received

- Rent paid minus 10% of salary

- 50% of salary (if residing in a metro city)

OR

40% of salary (if residing in a non-metro city)

“Salary” for this purpose generally includes:

- Basic salary

- Dearness allowance (if part of retirement benefits)

- Commission (if based on a fixed percentage of turnover)

The critical change lies in the third component – the percentage cap.

Numerical Illustration

Let’s compare the impact before and after the revision.

Scenario:

- Basic salary: ₹12,00,000 per annum

- HRA received: ₹6,00,000 per annum

- Rent paid: ₹5,40,000 per annum (₹45,000 per month)

Earlier (When Treated as Non-Metro – 40% Cap)

- 40% of salary = ₹4,80,000

- Rent paid – 10% of salary = ₹5,40,000 – ₹1,20,000 = ₹4,20,000

- Actual HRA received = ₹6,00,000

Exemption = Least of above = ₹4,20,000

Now (Treated as Metro – 50% Cap)

- 50% of salary = ₹6,00,000

- Rent paid – 10% of salary = ₹4,20,000

- Actual HRA received = ₹6,00,000

Exemption = ₹4,20,000

In this example, exemption does not change because rent minus 10% condition is limiting.

Higher Rent Scenario

If annual rent paid were ₹7,20,000:

- Rent minus 10% = ₹7,20,000 – ₹1,20,000 = ₹6,00,000

- 50% cap = ₹6,00,000

Now exemption = ₹6,00,000

Under earlier 40% cap, exemption would have been restricted to ₹4,80,000.

Additional tax-exempt amount = ₹1,20,000

For someone in the 30% tax bracket, this translates into tax savings of ₹36,000 (plus surcharge and cess impact).

Broader Economic Context

Cities like:

- Bengaluru – India’s technology and startup capital

- Hyderabad – Major IT and pharma hub

- Pune – Automotive, IT, and education center

- Ahmedabad – Manufacturing and financial growth hub

have experienced:

- Sharp increase in residential rentals

- Growing migrant professional workforce

- Expansion of corporate offices

- Rising cost of living

The revised classification aligns tax law with these ground realities.

Who Benefits the Most?

The biggest beneficiaries are:

- Mid-to-senior level professionals

- Employees with high HRA components

- Individuals paying substantial rent

- IT, startup, finance, and corporate sector employees

- Taxpayers opting for the old tax regime

Employees in premium rental localities stand to gain the most.

Impact on Employers and Payroll Structuring

Employers may now:

- Re-evaluate salary structuring strategies

- Optimize HRA components in CTC packages

- Provide better tax planning support to employees

For HR and payroll teams, updated metro classification ensures accurate tax deduction at source (TDS) calculations.

Interaction with Old vs New Tax Regime

A crucial point:

HRA exemption is available only under the old tax regime.

Taxpayers opting for the new tax regime cannot claim HRA exemption.

Therefore, employees in newly classified metro cities should reassess:

- Whether shifting to the old regime provides greater benefit

- Their overall deductions and exemptions

- Net tax payable under both regimes

A comparative computation is strongly advisable.

Compliance and Documentation Requirements

Despite the expansion, compliance standards remain unchanged:

- Rent receipts must be maintained

- PAN of landlord required if annual rent exceeds prescribed limits

- Genuine rental arrangement must exist

- HRA cannot be claimed if living in own house (with limited exceptions)

Proper documentation is essential to avoid scrutiny.

Policy Significance

This change demonstrates:

- Recognition of evolving metropolitan ecosystems

- Responsive tax policy

- Focus on salaried middle-class relief

- Modernization of outdated classifications

It also signals that tax administration is gradually adapting to India’s shifting urban and economic landscape.

Key Takeaways

- Metro city list expanded from 4 to 8

- Ahmedabad, Hyderabad, Pune, and Bengaluru now qualify

- 50% salary cap applies to these cities

- Formula for HRA remains unchanged

- Benefit available only under old tax regime

- Potential for meaningful tax savings

Conclusion

The expansion of recognized metro cities under the Income Tax Rules marks a significant shift in HRA computation. For employees living in Ahmedabad, Hyderabad, Pune, and Bengaluru, the 50% salary threshold can lead to increased exemption and lower taxable income — particularly in high-rent scenarios.

This update not only provides financial relief but also reflects the economic transformation of India’s emerging urban powerhouses.