The Income-tax Act of 1961 has been the backbone of India’s tax system for more than six decades. Over the years, countless amendments, notifications, and clarifications transformed it into a massive legal labyrinth with over 800 sections and 100,000+ words. Taxpayers, accountants, and even tax officers often struggled to keep up, leading to widespread confusion, compliance burdens, and an explosion of litigation.

In 2025, the government has introduced a rewritten Income-tax Act, reducing the number of sections to 536. The new law promises clarity, simplicity, and fairness, making tax administration easier for both taxpayers and authorities.

Let’s dive deep into the major changes and what they mean for you.

1. Fewer Sections, Clearer Language

One of the most noticeable changes is the reduction in the number of sections. Many provisions in the old law were either repetitive, obsolete, or scattered across multiple places.

- Consolidation of similar rules: For example, separate sections on depreciation, different classes of income, and penalties have been merged where possible.

- Removal of outdated provisions: Rules that applied to bygone business models, expired exemptions, or defunct industries have been deleted.

- Simpler drafting: The new Act uses plain, modern language instead of dense legal jargon, making it easier for ordinary taxpayers to read and understand without requiring legal expertise.

This isn’t just cosmetic, it reduces ambiguity and helps ensure that interpretation is uniform across cases.

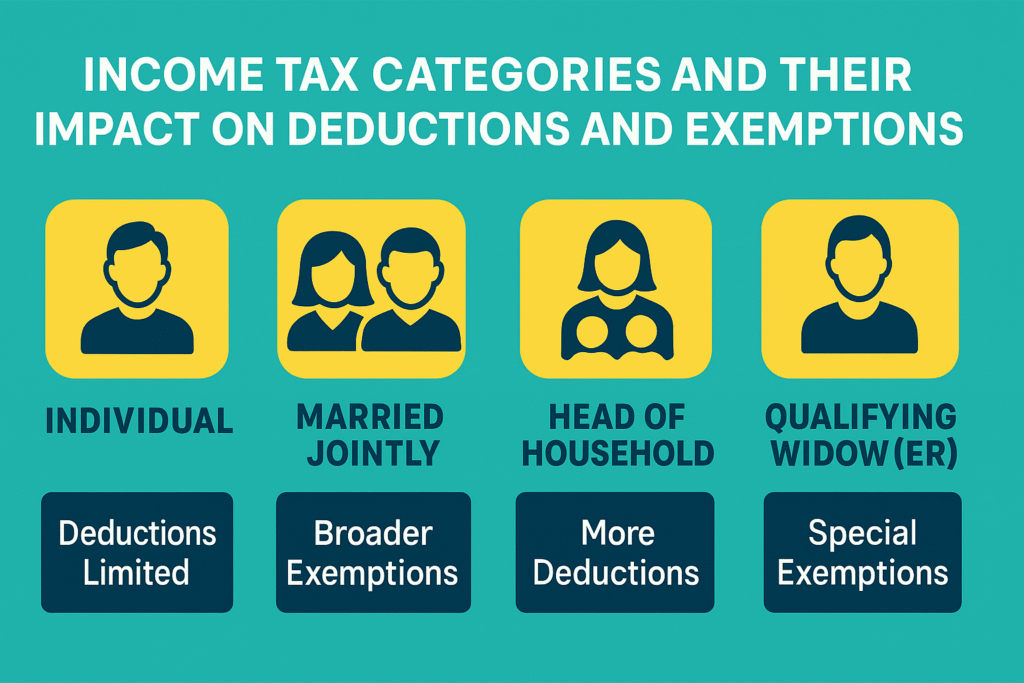

2. Broader Tax Exemptions and Rationalized Deductions

The government has raised exemption thresholds and rationalized deductions to simplify personal income tax.

- Higher basic exemption limit: The minimum income level at which tax applies has been increased, giving relief to lower- and middle-income earners.

- Special relief for seniors: Senior citizens and super-senior citizens enjoy higher exemption thresholds, reflecting their limited earning capacity.

- Streamlined deductions: Instead of dozens of overlapping allowances (like travel, medical, and meal vouchers), the new law consolidates them into a handful of broad deductions. This reduces paperwork and confusion while still rewarding saving and investment.

This reform ensures taxpayers spend less time tracking receipts and more time focusing on meaningful financial planning.

3. Faceless Assessments and Appeals as the Norm

Introduced a few years ago, faceless assessments are now fully embedded into the law. Under this system:

- Tax returns are selected for scrutiny by AI-driven algorithms, reducing bias.

- All communication is electronic—no in-person meetings with tax officers.

- Appeals and reviews also happen digitally, ensuring transparency and uniform treatment.

This change curbs opportunities for corruption and harassment while giving taxpayers confidence that their case will be judged on facts, not relationships.

4. Reduced Litigation and Faster Dispute Resolution

India’s tax system has historically generated enormous litigation, clogging up courts for decades. The rewritten law addresses this by:

- Eliminating grey areas: Ambiguous provisions (like the definition of “business connection” for international taxation) have been clarified.

- Clear timelines: Assessments, appeals, and refunds now have strict time limits, reducing uncertainty.

- Alternative Dispute Resolution (ADR): The law encourages conciliation, settlement schemes, and mediation panels to resolve issues outside courts.

This shift is crucial for improving India’s ease of doing business and reducing compliance anxiety.

5. Digital-First Compliance

The new Act embraces technology as the backbone of compliance.

- Pre-filled ITRs (Income Tax Returns): Salaried employees, pensioners, and small taxpayers will find most data already filled in from sources like Form 16, banks, and mutual funds.

- AI-based risk assessment: High-risk cases (like unexplained cash deposits or luxury spending mismatched with declared income) will be flagged automatically.

- Paperless filings: Almost all processes—from filing to refunds to appeals—are designed to be electronic.

This reduces dependence on intermediaries for simple filings and cuts compliance costs for ordinary taxpayers.

6. Simplified Corporate Tax Provisions

Businesses, especially startups and MSMEs, have often complained that corporate tax provisions were too complex. The rewrite focuses on:

- Merging incentive schemes: Instead of dozens of overlapping tax holidays and sector-specific benefits, the law offers a few broad incentive categories.

- Streamlined depreciation rules: Fewer asset classes, simplified depreciation rates, and easier calculation methods.

- Clearer transfer pricing guidelines: Reducing litigation around cross-border transactions by aligning rules with international standards.

This makes compliance predictable and transparent, allowing businesses to focus on growth instead of litigation.

7. A More Taxpayer-Friendly Framework

The rewritten Act isn’t just shorter; it’s designed around the taxpayer’s perspective. Key improvements include:

- Simpler forms with fewer schedules.

- Better grievance redressal mechanisms through dedicated ombudsmen.

- Time-bound refunds, ensuring taxpayers aren’t stuck waiting indefinitely.

By reducing complexity, the law aims to build trust between taxpayers and the tax department.

8. Stronger Focus on Anti-Evasion Measures

While the law is more taxpayer-friendly, it also strengthens safeguards against tax evasion.

- Tighter reporting of foreign income and assets ensures transparency in cross-border holdings.

- Stronger penalties for willful misreporting or failure to disclose critical information.

- Mandatory high-value transaction reporting (real estate, luxury cars, stock trades, crypto) to plug leakages.

This dual approach balances simplification for honest taxpayers with stricter compliance for those trying to game the system.

9. Alignment with Global Tax Practices

The new Act is drafted to bring India closer to global best practices in taxation.

- BEPS compliance (Base Erosion and Profit Shifting) aligns India with international corporate tax norms.

- Digital economy taxation rules clarify how global tech giants are taxed on revenues earned from Indian users.

- Advance pricing agreements (APAs) and safe-harbor rules reduce uncertainty in cross-border trade.

This makes India’s tax framework more compatible with international investors and improves ease of doing business.

10. Stability Through Fewer Amendments

One major complaint about the old law was frequent annual amendments through Finance Acts, making tax planning unpredictable. The rewritten law emphasizes:

- Stable provisions designed to last without yearly tinkering.

- Greater reliance on rules, not ad-hoc notifications, to implement changes.

- Clear sunset clauses for incentives and exemptions to avoid confusion.

This stability allows both individuals and businesses to plan long-term finances and investments with confidence.

What This Means for You

The rewrite of India’s income tax law is a landmark reform. It represents a shift from a complex, litigation-heavy system to one that is simpler, digital, and taxpayer-centric.

- For individuals, it means easier returns, higher exemptions, and fewer disputes.

- For businesses, it means clarity, reduced litigation, and predictable compliance.

- For the government, it means better tax collections, reduced administrative burden, and improved ease of doing business rankings.

The real success, however, will depend on smooth implementation and how effectively the transition is managed in practice.